Who is recognized as a tax agent for VAT (responsibilities, nuances). What transactions are made by a VAT tax agent? How to calculate VAT by a tax agent

In accordance with Art. 161 of the Tax Code of the Russian Federation, organizations can act as tax agents.

The program automates the following cases when organizations can act as tax agents:

- when leasing federal, municipal property or property of constituent entities of the federation from government or administrative bodies;

- when purchasing goods, works, services on the territory of the Russian Federation from foreign organizations that are not registered with the tax authorities of the Russian Federation;

- when purchasing state (municipal) property;

- when selling goods to foreign persons who are not registered with the tax authorities of the Russian Federation on the basis of commission agreements.

Tax agents are required to calculate, withhold from the taxpayer and pay the appropriate amount of VAT to the budget. This section uses an example to examine the reflection of an organization’s business operations when performing the duties of a tax agent when purchasing goods from a foreign organization that is not registered with the tax authorities of the Russian Federation.

To reflect transactions, you must do the following:

1. Registration of an agreement with the performance of duties of a tax agent.

Let's register the agreement in the directory "Contractors' Agreements":

- choose the type of contract - With a supplier,

- check the box "The organization acts as a tax agent for the payment of VAT",

- choose the type of agency agreement,

- Let's indicate the general name.

2. Transfer of advance payment

To do this, you need to register the document “Outgoing Payment Order” (menu “Documents - Cash”).

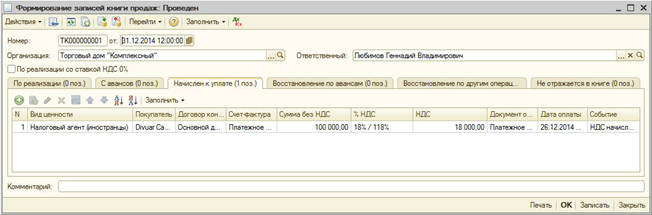

3. Registration of the issued invoice

When transferring payment to a supplier under an agreement with the performance of duties as a tax agent, you must issue an invoice.

An invoice can be generated automatically by processing "Registration of tax agent invoices" (menu "VAT - Registration of tax agent invoices") or entered manually based on the payment document.

Tax agent invoices are generated and posted by clicking the “Run” button. When processing occurs, invoices are created and the data of previously created invoices is updated.

When posting tax agent invoices, VAT amounts payable to the budget are calculated: an entry is made to the debit of account 76.NA “Calculations for VAT when performing the duties of a tax agent” and to the credit of account 68.32 “VAT when performing the duties of a tax agent.”

The amount of accrued VAT is reflected in the sales book.

In the invoice, the item is filled in with the generic name from the contract. The item name can be indicated manually on the invoice.

4. Receipt of goods

Let's register the document "Receipt of goods and services" with the type of operation "Purchase, commission" (menu "Documents - Purchasing"). To offset the advance payment with the supplier, we will perform the processing “Restoring the sequence of settlements with counterparties” (menu “Documents - Additional”).

Postings are generated:

5. Transfer of VAT to the budget

The fact of VAT transfer to the budget is registered by the document “Outgoing payment order” with the type of operation “Tax transfer” (menu “Documents - Cash”).

The document must indicate the counterparty, the agreement and the settlement document that was used to transfer the payment to the supplier.

6. Registration of the VAT amount in the purchase book

Purchase ledger entries for VAT deductible amounts when performing the duties of a tax agent are reflected in the document “Creating purchase ledger entries” on the “VAT deduction for tax agent” tab. The table part is automatically filled in using the "Fill" button.

When conducting, the following transactions are generated:

2. VAT

3. Mediation activities

Legal basis of the agency agreement.

The legal features of agency agreements are established by Chapter 52 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation).

In accordance with Article 1005 of the Civil Code of the Russian Federation:

“Under an agency agreement, one party (the agent) undertakes, for a fee, to carry out legal and other actions on behalf of the other party (the principal) on its own behalf, but at the expense of the principal or on behalf and at the expense of the principal.”

Depending on how it is concluded, the rights and obligations of each party to the contract differ.

Under a transaction made by an agent with a third party on his own behalf and at the expense of the principal, the agent acquires rights and becomes obligated, even if the principal was named in the transaction or entered into direct relations with the third party for the execution of the transaction.

In this case, the rules of Chapter 51 “Commission” of the Civil Code of the Russian Federation, that is, the rules of the commission agreement, are applicable to the relations arising from the agency agreement.

In a transaction concluded by an agent with a third party on behalf and at the expense of the principal, the rights and obligations arise directly from the principal.

In this case, the rules of Chapter 49 “Agreement of Agency” of the Civil Code of the Russian Federation are applicable. It should be borne in mind that if an agency agreement is implemented according to the scheme of an agency agreement, then the general rules on representation established by Chapter 10 “Representation” apply to it, as well as to the agency agreement. Power of attorney" of the Civil Code of the Russian Federation.

That is, an agency agreement is a form of intermediary agreement, which includes elements of a mandate agreement and a commission agreement.

Within the framework of one contract, an agent may be assigned instructions of a different nature: some he performs, speaking on his own behalf, others - on behalf of his principal.

The principal pays the agent remuneration in the amount and in the manner specified in the agency agreement. This provision is established by Article 1006 of the Civil Code of the Russian Federation. If the agency agreement does not provide for the amount of agency remuneration and cannot be determined based on the terms of the agreement, the remuneration must be paid in the amount in which, under comparable circumstances, similar services are usually paid.

At the same time, I would like to draw attention to the fact that in the absence of conditions in the contract on the procedure for paying the agency fee, the principal is obliged to pay the remuneration within a week from the moment the agent submits to him a report for the past period, unless a different payment procedure follows from the essence of the contract or business customs rewards.

According to Article 1007 of the Civil Code of the Russian Federation, the parties to an agency agreement may limit each other in certain rights. But this must be stated in the contract.

In accordance with Article 1007 of the Civil Code of the Russian Federation:

"1. An agency agreement may provide for the principal's obligation not to enter into similar agency agreements with other agents operating in the territory specified in the agreement, or to refrain from carrying out independent activities in this territory that are similar to the activities that form the subject of the agency agreement.

2. An agency agreement may provide for the agent’s obligation not to enter into similar agency agreements with other principals, which must be executed in the territory that fully or partially coincides with the territory specified in the agreement.”

Paragraph 3 of Article 1007 of the Civil Code of the Russian Federation prohibits the establishment of provisions in an agency agreement by virtue of which the agent has the right to sell goods, perform work or provide services exclusively to a certain category of consumers or exclusively to consumers located or living in the territory specified in the agreement. Such conditions are declared void.

During the execution of the agency agreement, the agent is obliged to submit reports to the principal in the manner and within the time limits provided for by the agreement. If there are no corresponding conditions in the contract, then reports are submitted by the agent as he fulfills the contract or upon expiration of the contract. This is determined by paragraph 1 of Article 1008 of the Civil Code of the Russian Federation.

Unless otherwise provided by the agency agreement, the agent's report must be accompanied by the necessary evidence of expenses incurred by the agent at the expense of the principal. The principal who has objections to the agent’s report must notify the agent about this within thirty days from the date of receipt of the report, unless a different period is established by agreement of the parties. Otherwise, the report will be considered accepted.

In accordance with Article 1009 of the Civil Code of the Russian Federation, unless otherwise provided by the agency agreement, the agent has the right, in order to fulfill the agreement, to enter into a subagency agreement with another person. In this case, the agent remains responsible for the actions of the subagent to the principal. Moreover, the agency agreement may provide for the agent’s obligation to enter into a subagency agreement, with or without indicating the specific terms of such an agreement.

The subagent has no right to enter into transactions with third parties on behalf of the person who is the principal under the agency agreement. The exception is cases when, in accordance with paragraph 1 of Article 187 of the Civil Code of the Russian Federation, a subagent can act on the basis of sub-confidence.

Paragraph 1 of Article 187 of the Civil Code of the Russian Federation establishes that:

“The person to whom the power of attorney has been issued must personally perform the actions for which he is authorized. It may entrust their execution to another person if it is authorized to do so by a power of attorney or is forced to do so by force of circumstances to protect the interests of the one who issued the power of attorney.”

The procedure and consequences of such reassignment are determined according to the rules provided for in Article 976 of the Civil Code of the Russian Federation.

Article 1010 of the Civil Code of the Russian Federation establishes the grounds according to which an agency agreement is terminated due to:

“refusal by one of the parties to fulfill an agreement concluded without determining the expiration date of its validity;

death of an agent, recognition of him as incompetent, partially capable or missing;

recognition of an individual entrepreneur who is an agent as insolvent (bankrupt).”

In accordance with Article 1011 of the Civil Code of the Russian Federation, the rules on a commission agreement (Chapter 51 of the Civil Code of the Russian Federation) or orders (Chapter 49 of the Civil Code of the Russian Federation) may be applied to relations arising from an agency agreement, if they do not contradict the norms of Chapter 52 “Agency” of the Civil Code of the Russian Federation and the essence agency agreement.

The rules provided for in Chapters 49 and 51 of the Civil Code of the Russian Federation apply depending on whether the agent acts under the terms of this agreement on behalf of the principal or on his own behalf. If the agent acts on behalf of the principal, then the rules of the contract of agency apply. If the agent acts on his own behalf, then the rules of the commission agreement apply.

The provision of services on the territory of the Russian Federation is subject to taxation with value added tax (hereinafter referred to as VAT). This is established by subparagraph 41 of paragraph 1 of Article 146 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation).

The tax base is determined in accordance with paragraph 1 of Article 156 of the Tax Code of the Russian Federation. In accordance with paragraph 1 of the said Article 156 of the Tax Code of the Russian Federation:

“Taxpayers, when carrying out business activities in the interests of another person on the basis of agency agreements, commission agreements or agency agreements, determine the tax base as the amount of income received by them in the form of remuneration (any other income) in the performance of any of these agreements.”

In the agent's accounting, revenue associated with the provision of intermediary services is income from ordinary activities. This is determined by paragraph 5 of the Accounting Regulations “Income of the Organization” PBU 9/99, approved by Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 32n (hereinafter referred to as PBU 9/99).

In the agent’s accounting, the amount of revenue from the provision of intermediary services is reflected in account 90 “Sales” subaccount 90-1 “Revenue” in correspondence with account 76-5 “Settlements with various debtors and creditors”. In this case, it is advisable to open a subaccount “Settlements with the principal” for account 76-5 “Settlements with various debtors and creditors”.

The agent's expenses related to the provision of intermediary services are recorded in the account. The amounts accumulated on account 26 “General business expenses” are written off to the debit of account 90 “Sales” subaccount 90-2 “Cost of sales”.

Let us note that depending on the subject of the agency agreement, the procedure for maintaining accounting records of intermediary transactions is distinguished. Conventionally, agency transactions can be divided into two groups:

Concluding contracts with buyers for the sale of goods (works, services) of the principal;

Concluding agreements with suppliers of material assets for the principal.

Let's look at examples of the procedure for reflecting intermediary transactions in the accounting records of an agent.

Example 1.

LLC "Principal" instructed LLC "Agent" to sell goods in the amount of 295,000 rubles (including VAT 45,000 rubles). According to the concluded agreement, the agency fee is 8% (including VAT) of the cost of goods sold and paid for by Principal LLC.

After the expiration of the agency agreement, Agent LLC submitted a report to Principal LLC, according to which the goods were completely sold.

In the example under consideration, the agent participates in the calculations.

Own expenses of Agenta LLC amounted to 2,500 rubles.

The working chart of accounts provides for the use of the following accounts:

|

Account correspondence |

Amount, rubles |

||

|

Debit |

Credit |

||

|

Received goods from LLC “Principala” for sale |

|||

|

76-5 “Settlements by the principal” |

The sale of goods to customers is reflected |

||

|

62-3 “Settlements with buyers and contractors under an agency agreement” |

Payment for goods by the buyer is reflected |

||

|

76-5 “Settlements with the principal” |

Agency fee accrued (RUB 295,000 x 8%) |

||

|

VAT charged on agency fees |

|||

|

Own expenses of Agent LLC are reflected |

|||

|

76-5 “Settlements with the principal” |

Funds were transferred to the Principal minus commission |

||

|

90-9 “Profit / loss from sales” |

The financial result of Agent LLC is reflected |

||

End of the example.

Example 2.

LLC "Principal" entered into an agency agreement with LLC "Agent" for the purchase of goods for it with delivery to the location of the warehouses of LLC "Principal". According to the agreement, the remuneration of Agent LLC is 3% of the transaction amount after approval of the report by Principal LLC.

Principal LLC transferred funds to Agent LLC for the purchase of goods and expenses associated with the purchase of goods in the amount of 944,000 rubles.

The working chart of accounts of Agent LLC opened the following subaccount for account 76 “Settlements with various debtors and creditors”:

76-5 “Settlements with the principal”

|

Account correspondence |

Amount, rubles |

||

|

Debit |

Credit |

||

|

76-5 “Settlements with the principal” |

Reflects the funds received from the principal for the execution of the contract |

||

|

60-1 “Settlements with suppliers and contractors under an agency agreement” |

Reflected prepayment to the supplier for the goods |

||

|

60-1 Settlements with suppliers and contractors under an agency agreement" |

Reflects prepayment to the transport company for delivery of goods |

||

|

76-5 “Settlements with the principal” |

60-1 “Settlements with suppliers and customers under an agency agreement” |

Report provided to the principal |

|

|

Reflected agency fee (696,200+147,800) x 3% |

|||

|

68-2 “Calculations for value added tax” |

VAT charged on remuneration |

||

|

76-5 “Settlements with the principal” |

The remaining amount of the prepayment from the principal is reflected against the accrued remuneration |

||

|

76-5 “Settlements with the principal” |

The remaining amount of the transferred prepayment was transferred to the Principal |

||

|

The agent's own expenses are reflected |

|||

|

90-9 “Profit and loss from sales” |

The agent's financial result is reflected |

||

End of the example.

In accordance with paragraph 2 of Article 249 of the Tax Code of the Russian Federation, income from the sale of an agent’s services for profit tax purposes is recognized as revenue from the sale of services, which is determined on the basis of all receipts associated with payments for services rendered, less taxes charged to the principal.

For taxpayers - agents who determine income and expenses using the accrual method for profit tax purposes, the date of receipt of income is the date of sale of services, determined in accordance with paragraph 1 of Article 39 of the Tax Code of the Russian Federation, regardless of the actual receipt of funds to pay for them (paragraph 3 of Article 271 of the Tax Code of the Russian Federation ).

For taxpayers - agents who determine income and expenses using the cash method, the date of receipt of income is the day of receipt of funds in bank accounts and (or) at the cash desk. This is confirmed by Letter of the Ministry of Finance of the Russian Federation dated March 15, 2006 No. 03-03-04/1/231.

According to Article 252 of the Tax Code of the Russian Federation:

In the previous section, we indicated that the principal can instruct the agent to either sell goods (work, services) or purchase goods (work, services).

In accounting, the principal reflects revenue only after receiving the agent’s report on the fact that he has fulfilled his obligations under the agency agreement. It is the agent’s report that confirms compliance with the conditions for revenue recognition in accounting specified in paragraph 12 of PBU 9/99:

“a) the organization has the right to receive this revenue arising from a specific agreement or confirmed in another appropriate manner;

b) the amount of revenue can be determined;

c) there is confidence that as a result of a particular transaction there will be an increase in the economic benefits of the organization. Confidence that as a result of a particular transaction there will be an increase in the economic benefits of the organization exists when the organization received an asset in payment or there is no uncertainty regarding the receipt of the asset;

d) the right of ownership (possession, use and disposal) of the product (goods) has passed from the organization to the buyer or the work has been accepted by the customer (service provided);

e) the expenses that have been incurred or will be incurred in connection with this operation can be determined.”

The principal uses account 45 “Goods shipped” to reflect goods transferred to the agent for sale. The operation of transferring goods to the agent is reflected in the principal’s accounting by transferring the corresponding amounts from the credit of account 41 “Goods” to the debit of account 45 “Goods shipped”.

After ownership of the goods is transferred to the buyer, the principal records the revenue in account 90 “Sales” subaccount 90-1 “Revenue”.

In some cases, the taxpayer is not the taxpayer himself, but the company to which he belongs. Often it is this company that pays the taxpayer's wages. The main company, at the same time, pays the tax not from its own pocket, but from funds that rightfully belong to the taxpayer. Therefore, accountants withhold tax from the profit that is due for payment and pay the amount with the VAT amount already calculated.

Who is a VAT tax agent?

At the same time, the company that actually pays the money is called the tax agent. To put it another way, it is she who acts as an intermediary between the company that received the actual profit and the tax service itself, which collects funds and transfers them to the budget. This way of handling money arose due to the fact that some organizations, for legal reasons, are not able to pay taxes on their own.

There are a number of situations in which the state imposes agent duties on a company. They are listed in Article 161 of the RF NU.

In simple terms, an insurance agent is considered to be:

- If you buy foreign-made goods, services or work that are registered in the Russian Federation. Moreover, the place of sale is located in Russia.

- If you rent premises from government agencies, or purchased it.

- If you are selling property that is tied to treasure hunting: coins or other treasure contents, or other wealth.

- If you acquire the property of an organization that has been declared bankrupt.

- If you are an intermediary who sells services or goods whose owners are not located in the Russian Federation.

- If, after the transfer of ownership rights to you, you managed to build a vessel, but did not have time to register it in the International Register of Ships.

What VAT entries are reflected in the tax agent’s accounts?

As for VAT, the accountant uses only two entries:

- Debit 90, Credit equal to 68 - indicates that VAT is charged on the sale of goods and services provided in the main activity of the enterprise.

- Debit 91, Credit equal to 68 - if tax was calculated on the sale of a certain product or service, for additional activities. For example, if a company produces dairy products and simultaneously rents out refrigeration equipment to stores.

Postings for processing input VAT:

- Debit 19, Credit equal to 60 is used to take into account taxes on purchased goods and services.

- Debit 68, Credit 19 is used if VAT on purchased goods and services is accepted for deduction.

To account for input VAT and write it off as expenses, the following entries are used:

- Debit 19, Credit equal to 60 - this scheme is used if VAT on purchased goods is taken into account.

- Debit 19, Credit equal to 60 - an entry that is used if the tax on goods is included in their cost.

In some cases, it is impossible to calculate VAT on a certain group of goods or services. For example, you purchase slot machines that will be used in the gambling business. It is not subject to taxes, so there is nothing to charge VAT on. In such cases, the tax can be added to the cost of the machine by hiding it there.

For transactions that are used to recover VAT:

- Debit 60, Credit 68 This entry is used to recover the tax from the advance payment transferred to it. In this case, the reason why VAT is restored does not matter.

- Debit 91, Credit 68 - used to restore VAT on the balance of goods when switching to a special regime, or if a company or enterprise has received tax exemption.

If a tax that was previously accepted for deduction needs to be returned, then a lot depends on the reason for this action

In order for VAT to be transferred to the country’s budget, there is only one entry: Debit 68, Credit 51.

When is VAT paid by the tax agent?

It is necessary to transfer tax to the budget if:

- If the transactions relate to property that belongs to the state.

- If the services are provided by an organization that is registered abroad.

The amount that must be transferred can be calculated in several ways. To calculate the amount of tax on foreign currency payments, it is necessary to correctly determine the transaction rate. Tax agents, who determine the tax base of an enterprise taking into account VAT, assess the tax for payment to the state treasury on the same day when the purchase of goods or receipt of services is made.

How to reflect VAT withholding?

Tax payment is required to be reflected in the financial statements. In order to fill out a VAT declaration to an agent, the issue must be approached with the utmost care and responsibility.

The declaration is submitted in electronic form. This must happen no later than the 25th day of the billing month, or at the end of the quarter.

Attention! Since January 2017, the declaration has been submitted on an updated form, which has been approved by the Federal Tax Service. Be sure to fill out the title page, where you carefully enter all the basic data. Before submitting the form, double-check the cover page.

Next, the agent must fill out paragraphs 1 and 2. If you are not a tax payer, then paragraph 12 will be added to the previous paragraphs. As for paragraph 2, dedicated to agent taxes, they must be filled out separately for each company in relation to which the tax payer considered an agent. This means that if you pay tax not for one organization, but for several, then you will need to fill out all the fields about each of them on a separate sheet.

In paragraph 3, line 180, the tax agent can indicate tax deductions after paying VAT to the country's budget. You can immediately fill out sections 2 and 3 if the purchase of goods or services and the payment of tax on this transaction occurred in the same billing period.

When drawing up a document, the tax agent must rely on the norms for calculating the tax base. The declaration is filled out on the basis of information from the book of sales and purchases, and information obtained from accounting registers.

When does the duty of a tax agent not arise?

But there are a number of situations in which a tax agent ceases to be considered as such. These include:

- If the purchase of property objects and persons who have been declared bankrupt is carried out. For example, if an organization purchases office furniture from a company declared bankrupt.

- In some cases, when concluding a lease agreement.

In such situations, all obligations to pay tax to the treasury are removed from the tax agent, and obligations to pay VAT do not affect his work.

Conditions for tax agent VAT deduction in 2016-2017

VAT paid by the agent can be credited to him. But in order to carry out this procedure, you need to decide on some questions that arise from the situation:

- Is the fact that the agent paid the tax even important?

- Is it necessary to capitalize the object, or is this procedure not necessary?

- Is it worth considering the place where the service was provided?

So, when filing a return as a tax agent, he should be extremely careful. You need to remember that the document must be submitted, like other taxpayers, before the 25th of the current month, or before the end of the billing period.

The declaration is submitted electronically and filled out in any place convenient for you where there is a computer and access to the Internet. Thanks to this service, you no longer need to stand in endless queues wasting time.

The tax agent fills out only the title page and paragraph 2.3 in the declaration. Most often, a tax agent acts as such not for one company, but for several. In this case, when filling out paragraph 2, you will need to work on several sheets, separate for each individual organization.

If the tax agent, for some reason, does not pay tax, or is exempt from it due to the nature of his activity, but at the same time regularly issues invoices to taxpayers, allocating a certain amount of tax, then he will need to fill out additional paragraph 12, in addition to the mandatory first section and title page.

In contact with

For an organization not registered in the Russian Federation, the company acts as a VAT agent (clauses 1 and 2 of Article 161 of the Tax Code of the Russian Federation). Buyers and tenants of the state and (Clause 3 of Article 161 of the Tax Code of the Russian Federation) also act.

At the same time, the departments note that the tax agent receives the right to deduct VAT only after paying the tax to the budget and accepting the purchased goods, works or services for registration (letters of the Ministry of Finance of Russia dated 06.21.13 No. 03-07-08/23545 and dated 11.29.10 No. 03-07-08/334, Federal Tax Service of Russia dated August 12, 2009 No. ShS-22-3/634@).

Also, a mandatory condition for deducting “agency” VAT is an invoice, which the agent issues independently within five calendar days (clause 3 of Article 168 of the Tax Code of the Russian Federation and letter of the Federal Tax Service of Russia dated August 12, 2009 No. ШС-22-3/634@).

How to reflect tax agent VAT in accounting

As a rule, in practice there are no difficulties when reflecting the tax agent’s VAT in the accounting records. Let's look at the situation using an example.

The company purchased a batch of construction materials from a foreign contractor not registered in the Russian Federation. She will make the following entries in her accounting:

DEBIT 41 CREDIT 60

— goods purchased from the counterparty are accepted for accounting;

DEBIT 19 CREDIT 60

— the amount of VAT under the contract is reflected;

DEBIT 60 CREDIT 68

— VAT is withheld from the amount of payment due to the supplier of goods, works, services;

DEBIT 60 CREDIT 51 (52)

— payment is transferred to the supplier of goods, works, services;

DEBIT 68 CREDIT 51

— “agency” VAT is transferred to the budget;

DEBIT 68 CREDIT 19

— “agency” VAT is accepted for deduction on the tax agent’s invoice.

If the subject of the contract is the performance of work or the provision of services (for example, rental of property), the first accounting entry will have the following form:

DEBIT 20 (26, 44, 91) CREDIT 76

— reflects the accounting expense as of the date of signing the acceptance certificate for work or services, including lease.

Let us note that if a company has entered into an agreement with a foreign counterparty, then the amounts of assets and liabilities must be recalculated for accounting purposes into rubles at the rate valid on the date of the transaction in foreign currency (clauses 4 and 6 of PBU 3/2006 “Accounting for assets and liabilities, the cost of which is expressed in foreign currency,” approved by order of the Ministry of Finance of Russia dated November 27, 2006 No. 154n).

What are the consequences of failure to withhold VAT by a tax agent?

Now, if a tax agent does not withhold and transfer the “agency” VAT to the budget, he faces liability under Article 123 of the Tax Code of the Russian Federation - a fine of 20% of the tax amount. Previously, this norm was formulated somewhat differently: from a literal reading of Article 123 of the Tax Code of the Russian Federation, it followed that liability arises if the tax agent did not transfer the tax to the budget.

It is important to remember that before the new edition of the Tax Code of the Russian Federation came into force, some courts declared it unlawful to hold liable a tax agent who failed to withhold tax from a counterparty. Thus, the Federal Antimonopoly Service of the North-Western District, in resolution dated November 17, 2005 No. A26-770/2005-28, recognized the sanctions of tax authorities as unlawful. The fact is that the foreign counterparty received income in kind. And the tax agent was not able to withhold the VAT due for payment to the budget. A similar decision was made by the Ninth Arbitration Court of Appeal in resolution dated September 14, 2012 No. 09AP-25217/2012-AK (upheld by resolution of the Federal Antimonopoly Service of the Moscow District dated December 18, 2012 No. A40-16152/12-90-73).

However, the majority of courts were of the opinion that inspectors have the right to hold a tax agent accountable regardless of whether he withheld the amount of VAT not paid to the budget (decision of the Constitutional Court of the Russian Federation dated 02.10.03 No. 384-O, resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated 28.02.01 No. 5, FAS Volga-Vyatsky dated 02.17.12 No. A43-7281/2011, Uralsky dated 05.11.10 No. Ф09-3355/10-С2 (left in force by the determination of the Supreme Arbitration Court of the Russian Federation dated 09.23.10 No. VAS-10832/10) and North -Kavkazsky dated September 25, 2008 No. F08-5634/2008 (left in force by the determination of the Supreme Arbitration Court of the Russian Federation dated September 23, 2010 No. VAS-10832/10) districts). Now this position is enshrined at the legislative level.

R. Yuropov,

Advisor to the State Civil Service of the Russian Federation, 3rd class

For unlawful non-withholding and (or) non-transfer of tax amounts by a tax agent, a tax sanction is provided - a fine in the amount of 20% of the tax amount. To avoid tax penalties, check your counterparties and transactions with them.

Below is a diagram that will help you figure out who is considered a tax agent for VAT.

Article 161 of the Tax Code of the Russian Federation describes situations when a tax agent calculates and pays VAT to the budget on behalf of a payer. Let's consider the two most popular situations.

Situation 1. Sales of goods, works, and services by foreign organizations in Russia

If a foreign organization has a representative office in Russia, then such an organization will calculate the VAT itself, pay it to the budget and issue you an invoice. If there is no representative office in the Russian Federation, then the buyer of goods, works, services will have to calculate VAT and withhold it from the amount paid to the foreign seller. Therefore, when concluding an agreement with a foreign organization, it is necessary to check the presence of a representative office or branch of the foreign organization in Russia.To confirm that you do not have duties as a tax agent, it is best to request a copy of the tax registration certificate (indicating the Taxpayer Identification Number and Taxpayer Identification Number) of the representative office of a foreign organization in Russia.

At the same time, if the buyer enters into a contract with the head office of a foreign company (a branch registered in the Russian Federation does not take part in the transaction), then the buyer must fulfill the duties of a tax agent, despite the presence of registration of a representative office in the Russian Federation (letter from the Ministry of Finance of Russia dated November 12, 2014 No. 03-07-08/57178).

If a foreign organization sells goods, works, or services that are not recognized as subject to VAT in Russia, then the buyer does not need to calculate and withhold VAT.

The tax to be withheld from payments to a foreign organization is calculated using the formula:

Example. A foreign organization provides information services to a Russian organization. In accordance with Art. 148 of the Tax Code of the Russian Federation, the Russian Federation is recognized as the territory for the provision of services. Foreign partners did not provide a certificate of registration with the tax authority in the Russian Federation. The cost of the service is 100,000 rubles. A Russian organization is required to withhold VAT when paying for services. The VAT amount will be 100,000*18/118 = 15,254.24 rubles. The executor under the contract will receive 84,745.76 rubles “in hand”.

Often, foreign counterparties indicate in contracts that they wish to receive a certain fixed amount of money for their goods, work, services, and the buyer must accrue all taxes payable in Russia in excess of the specified amount and pay at his own expense.

Such wording in agreements does not affect the manner in which the tax agent performs its functions and does not prevent the receipt of a deduction for VAT paid to the budget under such an agreement.

In a number of cases, Russian organizations are required to withhold from payments to foreign companies not only VAT, but also income tax (Article 309 of the Tax Code of the Russian Federation). If an organization is simultaneously a tax agent for both VAT and income tax, then taxes are calculated as follows: first, VAT should be calculated and withheld, and then income tax, excluding the VAT amount from the tax base.

For example, a Russian company pays a foreign company the cost of property rights to use the developed website 100,000 euros. VAT = 100,000 *18/118 = 15,254.24 euros. Income tax = (100,000 -15,254.24) * 20% = 16,949.15 euros. Tax amounts are recalculated into rubles at the exchange rate on the date of transfer to the budget (Article 45 of the Tax Code of the Russian Federation). Please note that the tax rate on the income of a foreign organization depends on the international agreement on the avoidance of double taxation between the Russian Federation and the country of which the foreign counterparty is a resident. The agreement may provide for the exemption of income of a foreign organization from taxation on the territory of the Russian Federation or taxation at a reduced tax rate. If there is no such agreement between states, then a rate of 20% should be applied.

According to Article 312 of the Tax Code of the Russian Federation, in order to apply exemption from taxation of income of a foreign company on the territory of the Russian Federation or to apply reduced tax rates, documentary evidence is required:

Residence in a country with which Russia has entered into an international agreement on the avoidance of double taxation;

The actual right to dispose of income received under the agreement (in particular, confirmation that the counterparty is not an intermediary).

Supporting documents must be provided by the foreign organization to the tax agent before the date of payment of income.

Situation 2. Provision of federal, municipal property, property of constituent entities of the Russian Federation by state authorities and management bodies, local self-government bodies

When concluding a lease agreement for state or municipal property, you must pay attention to who is the lessor under the agreement. The following options for concluding lease agreements are possible:1) Lessor - city administration, state property management committee, municipality or other similar body (bilateral agreement). In this case, the tenant is recognized as a tax agent.

2) Lessor - city administration, state property management committee, municipality or other similar body, balance holder - unitary institution (tripartite agreement). In this case, the tenant is also recognized as a tax agent.

3) Lessor - a municipal or federal unitary institution (school, hospital, bus station, etc.). Such institutions are independent taxpayers. The tenant is not a tax agent.

4) The lessor is a government institution. The services of such institutions are not subject to VAT. The tenant is not a tax agent.

If the tenant is a tax agent, then he is obliged to calculate VAT at the time of payment of rent. The tax amount is determined as follows:

Deadlines for paying VAT to the budget

When purchasing works or services from a foreign partner, tax payment to the budget is made by tax agents simultaneously with the payment of funds to the foreign partner. Banks will not accept a payment to a foreigner without a payment order to pay VAT to the budget (Article 174 of the Tax Code of the Russian Federation). When purchasing goods from foreign organizations, the tax must be transferred to the budget in equal parts no later than every 25th day within three months following the tax period in which the tax was calculated.The same deadlines are established for the transfer to the budget of VAT accrued in relation to rent for the use of state / municipal property.

In practice, it is more convenient for a tax agent to transfer VAT to the budget when making any purchase at the time of payment under an agreement with a foreigner or a government agency / municipality. This will allow you to avoid technical errors, and therefore avoid the accrual of penalties and fines for late transfer of tax to the budget. In addition, the payment period affects the period for deducting the amount of VAT paid to the budget by the tax agent.

Invoices

The tax agent issues an invoice no later than 5 calendar days after payment for goods, works, services (the sale of which is recognized as subject to VAT on the territory of the Russian Federation) in two copies. One copy is registered in the sales book, the second - at the moment the right to deduction arises in the purchase book.In lines 2, 2a, 2b of the invoice, the tax agent indicates the details of the seller/lessor. In line 2b (TIN and KPP) of the invoice, dashes are added if the seller is a foreign organization. In line 5 of the invoice, if works or services are purchased from a foreign organization, the tax agent must indicate the number and date of the payment order that transferred VAT to the budget.

Deductions

Persons who are recognized as tax agents in the situations described above are required to submit VAT returns to the tax authorities, regardless of whether they themselves are VAT taxpayers or not. At the same time, tax agents who are VAT payers can accept the paid VAT as a deduction. Agents who are not VAT payers cannot claim VAT for deduction, but have the right to include the amount of VAT paid in the cost of purchased goods, works, and services.Mandatory conditions for accepting VAT for deduction:

1) there are payment documents confirming the payment of VAT to the budget;

2) goods (work, services) for their use in activities subject to VAT;

3) there is an invoice issued by you (the tax agent);

4) purchased goods (works, services) are accepted for accounting. VAT can be deducted in the same period in which VAT is paid to the budget, subject to other mandatory conditions.

Example: The organization rents premises from the municipality to accommodate an office for 300,000 rubles. per month. The VAT amount is 300,000 * 18/118 = 45,762.71 rubles. The share of transactions subject to VAT is 5% of total revenue (clause 4 of Article 170 of the Tax Code of the Russian Federation). On March 30, the organization transfers 254,237.29 rubles to the budget. towards the rent for March and RUB 45,762.71. towards payment of VAT. The corresponding rental payments have been accrued in the accounting records. When generating a declaration for the 1st quarter, the organization will reflect: - the accrual of tax payable as a tax agent in the amount of 45,762.71 rubles, - the amount of VAT deductible in the amount of 2,288.14 rubles. (45762.71 *5%). The difference between the VAT paid to the budget and the VAT accepted for deduction (RUB 43,474.57) will be taken into account by the organization when calculating income tax as part of the costs of renting premises.

Thus, by concluding an agreement with a foreign organization or government authority (municipality), the organization (entrepreneur) assumes additional functions and responsibilities. In order to plan tax consequences, before signing an agreement with an “unusual” counterparty, you should first research its status, assess how its status will affect the calculation of taxes, and stock up on the necessary documents and confirmations.